Last updated on February 14th, 2026

Editor’s Note

In recent years, the narrative of a so-called Chinese “debt-trap diplomacy” has been repeatedly circulated in international discourse, yet in most cases, conclusive evidence of such an “intentional trap” is lacking. Currently, with the regular convening of the Forum on China-Africa Cooperation, ongoing adjustments to the Belt and Road Initiative (BRI), and the release of numerous academic and think-tank research reports, the trend in international discussion is shifting from confrontational narratives toward more practical issues of debt sustainability and management. This article examines two highly circulated social media claims which emerged in 2025, aiming to foster a more rational understanding of this topic among the international community.

Claim

In late July 2025, U.S. Senator Ted Cruz (R-Texas) posted on the social media platform X, stating: “For years, China has worked to lock up Africa’s critical minerals sector.” He further alleged that “China uses infrastructure loans to debt-trap African nations, then uses that debt to gain mining rights.”

Link to post

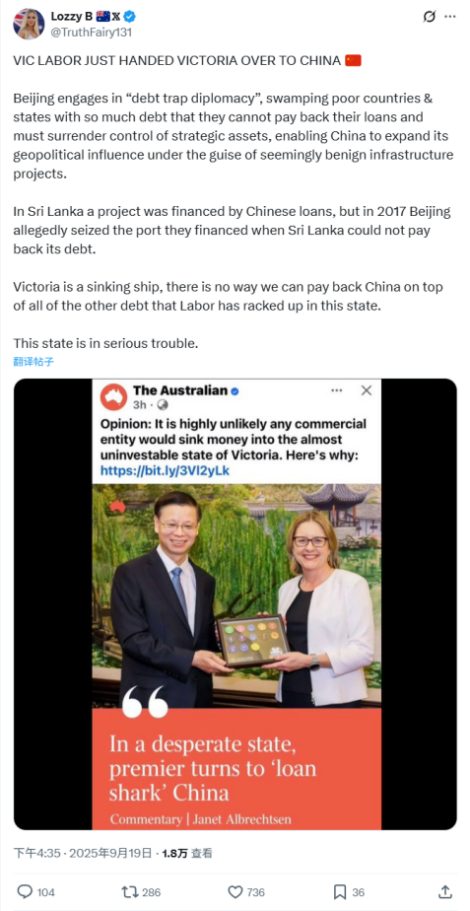

In September 2025, an Australian right-wing figure, in a post criticizing the Victoria state Labor government’s interactions with China, used political rhetoric to link the international case of Sri Lanka to local affairs, claiming: “In Sri Lanka a project was financed by Chinese loans, but in 2017 Beijing allegedly seized the port they financed when Sri Lanka could not pay back its debt.”

Link to post

Both claims garnered significant attention and shares, reflecting the continued resonance of the so-called “debt trap” narrative in certain discourse spheres.

Fact Check

1.Does China create “debt traps” through its loans?

Allegations of a “debt trap” are often linked to debt issues in countries like Sri Lanka and Zambia. However, data shows that debt crises in these countries are primarily caused by a combination of internal economic structural problems and external shocks, not solely by Chinese loans.

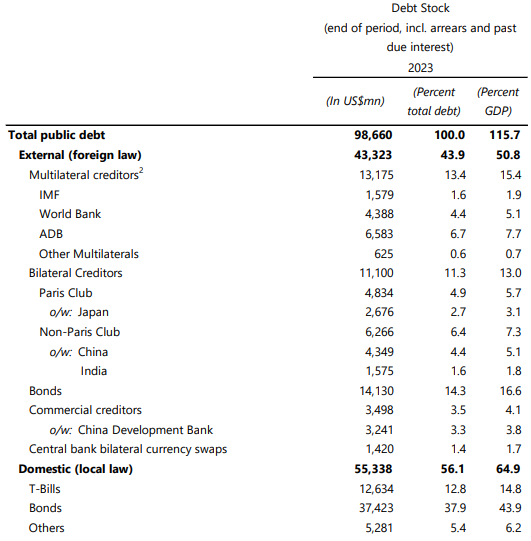

Taking Sri Lanka as an example, debt sustainability analyses from the International Monetary Fund (IMF) highlight that over 50 percent of the country’s external debt stems from high-cost sovereign bonds on international markets—the primary source of repayment risk. In contrast, bilateral debt to China constitutes about 10 percent, a share that is neither unusual for a major development partner nor, according to comparative debt analysis, high enough to be the determining factor in a sovereign debt crisis. For countries like Pakistan and Ethiopia, World Bank data consistently shows China is among several significant bilateral creditors, with its loan share often comparable to or less than that of other traditional partners.

In practice, China has repeatedly participated in debt restructuring and relief for partner countries. For instance, in 2022, China announced the cancellation of 23 interest-free loans due by the end of 2021 for 17 African countries. These measures align more with risk-sharing and flexible adjustment within cooperative frameworks than with a systematic strategy of setting “traps.”

2.Does China use debt to gain mining rights?

Although the narrative of “debt-trap diplomacy” is widely discussed, in most cases there is a lack of conclusive evidence proving the intentional setting of a “trap.” In reality, such cooperation is often a mix of resource-backed financing, project finance, and market logic, and does not constitute a systematic “debt-for-resources” model. Critics often describe this financing as “predatory,” but its nature is closer to development finance in high-risk environments.

President Cyril Ramaphosa of South Africa clearly stated in 2024 that China is not pushing Africa into a debt trap. Academic research also indicates that the sustainability of such cooperation varies by country, and no widespread, fixed “debt-for-mining” template exists. A 2023 report by the International Institute for Strategic Studies (IISS) also notes that China has demonstrated flexibility in practice, such as restructuring loans for Ethiopia’s railway, suggesting an approach geared toward risk-sharing and collaborative adjustment rather than unilateral asset seizure.

3.Does China gain control over strategic assets in BRI countries through debt?

Fact-checking shows that the claim that “China gains control over strategic assets through debt” does not align with the facts. Taking the frequently cited case of Sri Lanka’s Hambantota Port, the transfer of operational rights was based on a commercial lease agreement, not a seizure due to debt default.

According to official information from both China and Sri Lanka, sovereignty over the port always remains with Sri Lanka. Chinese companies only hold operational rights for the agreed lease period.

Similarly, cooperation on Pakistan’s Gwadar Port follows a comparable model. China provides funding and technical support in the building of the port, while Pakistan provides the land and formulates supporting policies. Operational rights are transferred based on an agreement. Full sovereignty over the port remains with Pakistan; there is no transfer of sovereignty due to debt issues.

These cases indicate that the relevant cooperation falls within the scope of common international commercial and infrastructure partnerships and does not undermine the host country’s sovereign control over strategic assets.

4.Are BRI loan terms harsh and non-transparent?

(1)Interest Rates: Are Chinese loans “harsh” due to high interest rates and fixed repayment schedules?

The interest rates on loans China provides to developing countries (approximately 2-3 percent) are higher than the concessional rates offered by multilateral institutions like the IMF (0.25-2 percent) but are significantly lower than international commercial bond rates (typically between 6%-10 percent%). For high-risk developing countries, loan interest rates that match project risk are in line with international market logic.

(2)Loan Model: Are Chinese loans often criticized for being “non-transparent” with “excessive confidentiality clauses”?

Chinese loans often adopt a “bilateral negotiation + commercialized” model, with most being commercial loans provided by state-owned enterprises. Confidentiality clauses in contracts are a routine part of international commercial practice. Furthermore, China respects the sovereign decisions of borrowing countries; some confidentiality requirements are actively requested by borrowing nations to maintain their own negotiating position.

5.What caused Sri Lanka’s debt crisis?

According to the IMF’s decomposition data on Sri Lanka’s public debt, its debt crisis was not primarily caused by borrowing from China. While China is an important bilateral creditor, the dominant share of Sri Lanka’s overall external debt comes from international capital markets (such as sovereign bonds and Eurobonds), multilateral institutions, and commercial creditors.

A report from the UK’s Overseas Development Institute (ODI) further concludes that the roots of Sri Lanka’s debt crisis lie in long-term structural fiscal imbalances, heavy reliance on international capital markets for high-cost financing, and the combined impact of external economic shocks.

6.Are debt troubles in other countries primarily due to Chinese loans?

While China is Africa’s largest bilateral lender, the causes of debt crises in developing countries are often complex and multifaceted, involving domestic economic structures, global market fluctuations, and the policies of multilateral institutions. They cannot be simplistically attributed to a single creditor.

Taking sub-Saharan Africa as an example, as of 2023, debt to China accounted for about 15 percent of the region’s total external debt, with the majority coming from international capital markets, multilateral institutions, and other bilateral creditors. Chinese loans are mostly used for infrastructure projects, with some backed by resource revenues for repayment, such as Angola’s “oil-for-loans” model. Such resource-backed arrangements are common internationally and are not unique to China, as evidenced by similar practices historically employed by France, Japan, Russia, and Western export credit agencies.

It is noteworthy that debt crises in many struggling countries are often closely related to other types of international borrowing. For instance:

6.1 Argentina (2018): An economic crisis was mainly triggered by currency collapse, fiscal imbalances, and over-reliance on international capital markets. The fiscal austerity policies implemented to secure a 57 billion U.S. dollar IMF bailout exacerbated recession and social unrest. [Source: BBC]

6.2 Zambia (2020): The country became Africa’s first sovereign defaulter during the pandemic. Its debt accumulation was related to global copper price volatility and years of borrowing from multiple sources. Despite receiving aid loans from the World Bank and IMF with attached austerity reforms, default was not prevented. [Source: BBC]

6.3 Lebanon (2020): A debt crisis stemmed from long-term domestic governance imbalances and fiscal mismanagement. IMF-demanded fiscal austerity and financial liberalization reforms failed to save its economy from collapse. [Source: IMF]

6.4 Egypt (2016): Energy subsidy cuts and currency devaluation policies were implemented to secure a 12 billion U.S. dollar IMF loan. While finances stabilized in the short term, living cost significantly increased. [Source: The Guardian]

6.5 Ukraine (2014): IMF loans accepted amid an economic recession and conflict came with conditions like fiscal austerity and energy price hikes, increasing social pressure in the short term. [Source: IMF]

These cases demonstrate how debt crises are typically the result of a combination of factors such as internal economic vulnerabilities, external shocks, and international financial conditions creating the perfect storm. Blaming such structural difficulties solely on Chinese loans not only overlooks the economic governance challenges within debtor nations themselves but also ignores the critical role played by international multilateral institutions and Western commercial creditors in many debt crises. Rational analysis of debt issues should be based on a comprehensive and balanced assessment of debt composition, not on a one-sided emphasis of a single source.

7.Analysis of Online Comments

Given the vast amounts of data across social media platforms, we employ AI-powered social analysis tools to assist in the analytical process. However, all our findings are subject to a strict verification, assessment, and final determination by human fact-checkers. Due to the dynamic nature of social media posts, we conducted two rounds of data collection and analysis—in December 2025 and January 2026—to more accurately assess engagement trends specifically for the July 2025 post published by Ted Cruz. The information presented below reflects data publicly accessible via the front end of the X platform as of the respective cutoff dates for each analysis.

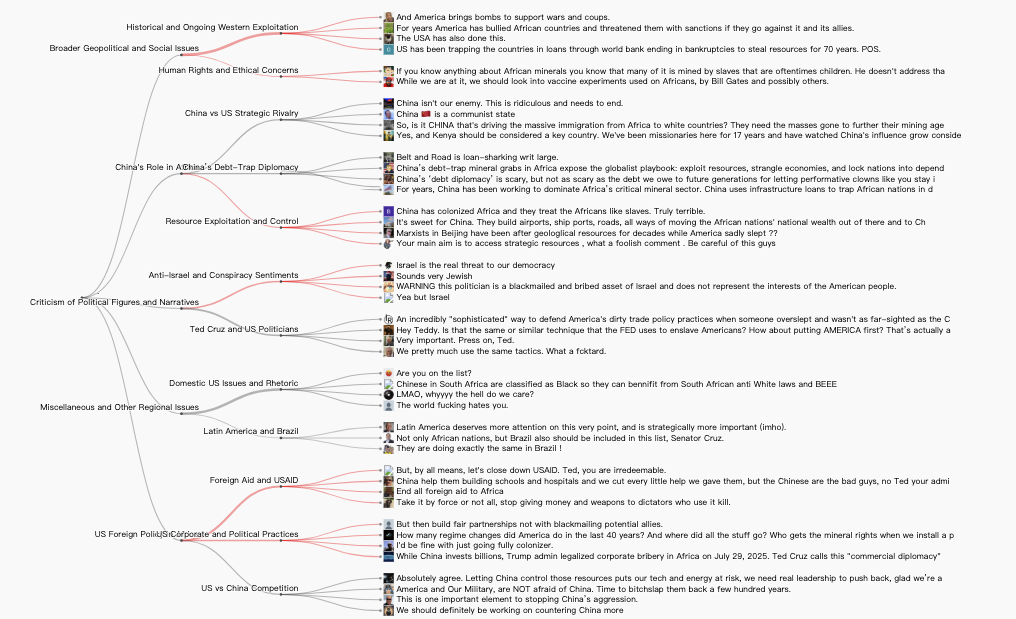

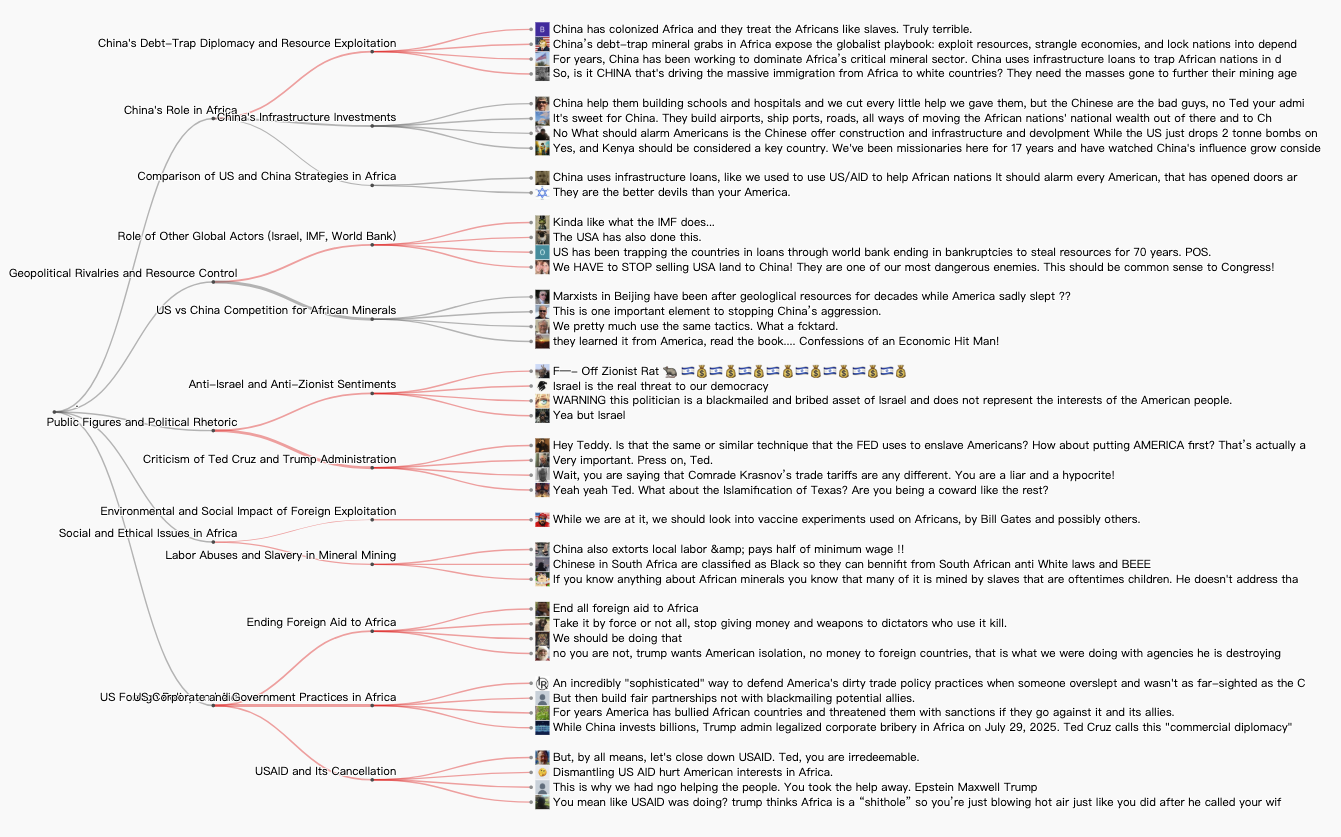

As of December 19, 2025, the post by U.S. Senator Ted Cruz had garnered 192 replies, with a total view count of 11,663, 326 likes, 34 retweets, and 26 replies.

Key discussion points: The tweets debated U.S. and Chinese competition strategies in Africa’s critical minerals sector, focusing on concerns about Chinese debt-trap diplomacy, insufficient U.S. investment, corporate corruption repackaged as “commercial diplomacy,” and calls to prioritize U.S. interests. The comments primarily expressed criticism and distrust of U.S. foreign policy in Africa, accusing the U.S. of exploiting African nations through debt traps, corruption, and resource extraction. Many comments exposed what they saw as hypocrisy in the U.S. actions, contrasting them with Chinese investments, and accused the U.S. of neglect, bullying, and perpetuating neocolonial practices. Furthermore, the comments were filled with strong dissatisfaction with Senator Ted Cruz, accusing him of supporting harmful policies, being influenced by foreign interests, and failing to address human rights violations.

As of January 16, 2026, Cruz’s post had garnered 192 replies, with a total view count of 10,884, 321 likes, 19 retweets, and 16 replies.

Key discussion points: The posts directed at Senator Cruz overwhelmingly express criticism and distrust regarding U.S. foreign policy in Africa and beyond. There is strong condemnation of American aid practices, alleged corporate bribery, and resource plundering, with some posts highlighting historical and ongoing abuses. Several comments also include harsh language and personal attacks, reflecting frustration and anger. Many focused on the perceived failures, double standards, and harmful consequences of U.S. policies.

Background

The term “Debt-Trap Diplomacy” originated from an article titled “China’s Debt-Trap Diplomacy” published in 2017 by Indian strategic scholar Brahma Chellaney, then a researcher at the Centre for Policy Research in New Delhi. The article was the first to explicitly link China’s Belt and Road Initiative (BRI) with the practice of acquiring strategic assets through large loans. The main allegations were based on cases like Sri Lanka’s Hambantota Port and Pakistan’s Gwadar Port.

In May 2025, the U.S. State Department launched a “Commercial Diplomacy Strategy,” which explicitly identified China as an economic and strategic competitor in Africa, and aimed to counter Chinese influence through commercial diplomacy. In July of the same year, the U.S. Embassy in The Bahamas issued a statement maliciously attacking the China-Bahamas “Nassau New Hospital Concessional Loan Project” and attempting to spread the “debt trap” theory, once again demonstrating the close link between this issue and geopolitical competition.

Summary

The statement by U.S. Senator Ted Cruz is a mixture of factual elements and interpretive assertions, generally consistent with U.S. foreign policy rhetoric highlighting competition with China. While the focus on mineral dominance and U.S. countermeasures may find some support, the “debt trap” allegation is more nuanced and has not been clearly proven as a systematic strategy.

Verdict

Misleading. The allegations by Senator Ted Cruz and others are misleading. Their arguments exhibit three common problems:

- Out of Context: Distorting commercial leases and normal operational cooperation into “loss of sovereignty.”

- Exaggerated: Using isolated cases like Hambantota Port to launch generalized attacks against the entire Belt and Road Initiative.

- Misattributed: Deliberately exaggerating the debt pressure of specific countries and attributing it solely to Chinese loans, completely ignoring core factors such as the debtor nations’own economic structures, governance issues, over-reliance on Western capital markets, and global macroeconomic shocks.

Current evidence suggests that the so-called “debt trap” functions more as a political label stemming from geopolitical competition motives rather than an objective conclusion based on comprehensive facts. Debt issues in international cooperation should be discussed rationally based on respect for facts and a comprehensive assessment of debt structures and cooperation terms.

Have a questionable video or claim? Submit it to Fact Hunter’s investigation team at [therealfacthunter@outlook.com].

– Fact Checker

– Primary Fact Checker: Liao Qin

– Secondary Fact Checker: SUN Chenghao, WAN Dai

Reference

https://lankatruth.com/si/wp-content/uploads/2024/07/IMF-report-2024-June_page-44.pdf

https://odi.org/en/publications/sri-lanka-from-debt-default-to-transformative-growth/

https://www.bbc.com/news/business-44408495

https://www.imf.org/en/countries/lbn/faq

https://www.theguardian.com/world/2016/nov/03/egypt-devalues-currency-meet-imf-demands-loan

International Monetary Fund. European Dept. “Ukraine: First Review Under the Stand-By Arrangement, Requests for Waivers of Nonobservance and Applicability of Performance Criteria, and A Request for Rephasing of the Arrangement”, IMF Staff Country Reports 2014, 263 (2014), accessed 2026/1/16, https://www.imf.org/external/pubs/ft/scr/2014/cr14263.pdf

https://www.imf.org/external/pubs/ft/dsa/lic.html